Calculating car registration fees is one of the most important steps when importing a car from Germany. The customs duty amount does not depend on the purchase price of the car, but from the pre-tax retail value, anti-pollution technology, CO emissions2 and the age of the vehicle.

It is the pre-tax price (LTPF) in which an identical car with the same equipment level was sold in Greece on the date of the first release of the car to be imported. This price is not the price we buy the car at and has nothing to do with the purchase invoice.

Car taxation is graduated with a different customs clearance rate depending on the value, as we see analyzed below:

For value from 0 until 14.000 € with customs clearance rate 4%

For value from 14.000 € until 17.000 € with customs clearance rate 26%

For value from 17.000 € until 20.000 € with customs clearance rate 53%

For value from 20.000 € until 25.000 € with customs clearance rate 62%

For value from 25.000 € until 30.000 € with customs clearance factor 71%

For value from 30.000 € and above with customs clearance rate 30%

This means that a car with a pre-tax retail value of €15,000 is taxed up to €14,000 at the rate of €14,000 (4%) and for the remaining €1,000 at the rate of the category €14,000-17,000 (26%).

The registration tax rate that a car must pay increases for cars with older anti-pollution technology than that considered the most modern.

At this moment as first anti-pollution category are considered euro6 cars with first registration INDICATIVELY from 31/8/2018 to date.

For value from 0 until 14.000 € with customs clearance rate 4%

For value from 14.000 € until 17.000 € with customs clearance rate 26%

For value from 17.000 € until 20.000 € with customs clearance rate 53%

For value from 20.000 € until 25.000 € with customs clearance rate 62%

For value from 25.000 € until 30.000 € with customs clearance rate 71%

For value from 30.000 € and above with customs clearance rate 30%

In the second antipollution category Cars that belong to the Euro6 category and have a first registration certificate are classified INDICATIVELY from 31/8/2015 to 31/8/2018 with customs clearance rates being increased by 50%, so they are formed as follows:

For value from 0 until 14.000 € with customs clearance rate 6%

For value from 14.000 € until 17.000 € with customs clearance rate 39%

For value from 17.000 € until 20.000 € with customs clearance rate 79,5%

For value from 20.000 € until 25.000 € with customs clearance rate 93%

For value from 25.000 € until 30.000 € with customs clearance rate 106,5%

For value from 30.000 € and above with customs clearance rate 45%

In the third category Cars that belong to the euro6a or euro5b category and first registration are classified INDICATIVELY from 31/12/2012 to 31/8/2015, with the customs clearance rates being increased by 100%, so they are structured as follows:

For value from 0 until 14.000 € with customs clearance rate 8%

For value from 14.000 € until 17.000 € with customs clearance rate 52%

For value from 17.000 € until 20.000 € with customs clearance rate 106%

For value from 20.000 € until 25.000 € with customs clearance rate 124%

For value from 25.000 € until 30.000 € with customs clearance rate 142%

For value from 30.000 € and above with customs clearance rate 60%

In the fourth category Cars belonging to the Euro5a category with a first registration from 31/12/2012 and below with customs clearance rates being increased by 200%.

Finally, in addition to the registration fee, cars with Euro4 anti-pollution technology are subject to an environmental fee of €3,000, while cars with Euro5 anti-pollution technology are subject to an environmental fee of €1,000.

OBSERVATION:

The above does not mean that when we import a second generation Euro6 car we will pay more customs duty compared to a third generation Euro6 car. The reason is that the second generation Euro6 will be cleared with a higher customs clearance rate compared to the third generation Euro6, but it will have a greater impairment due to age and may ultimately result in lower customs duty.

The emitted mass of carbon dioxide will affect the registration fee coefficient, which will increase with increasing grams according to the list below:

3.1 For cars with first registration before 1/1/2021

3.2 For cars with first registration after 1/1/2021

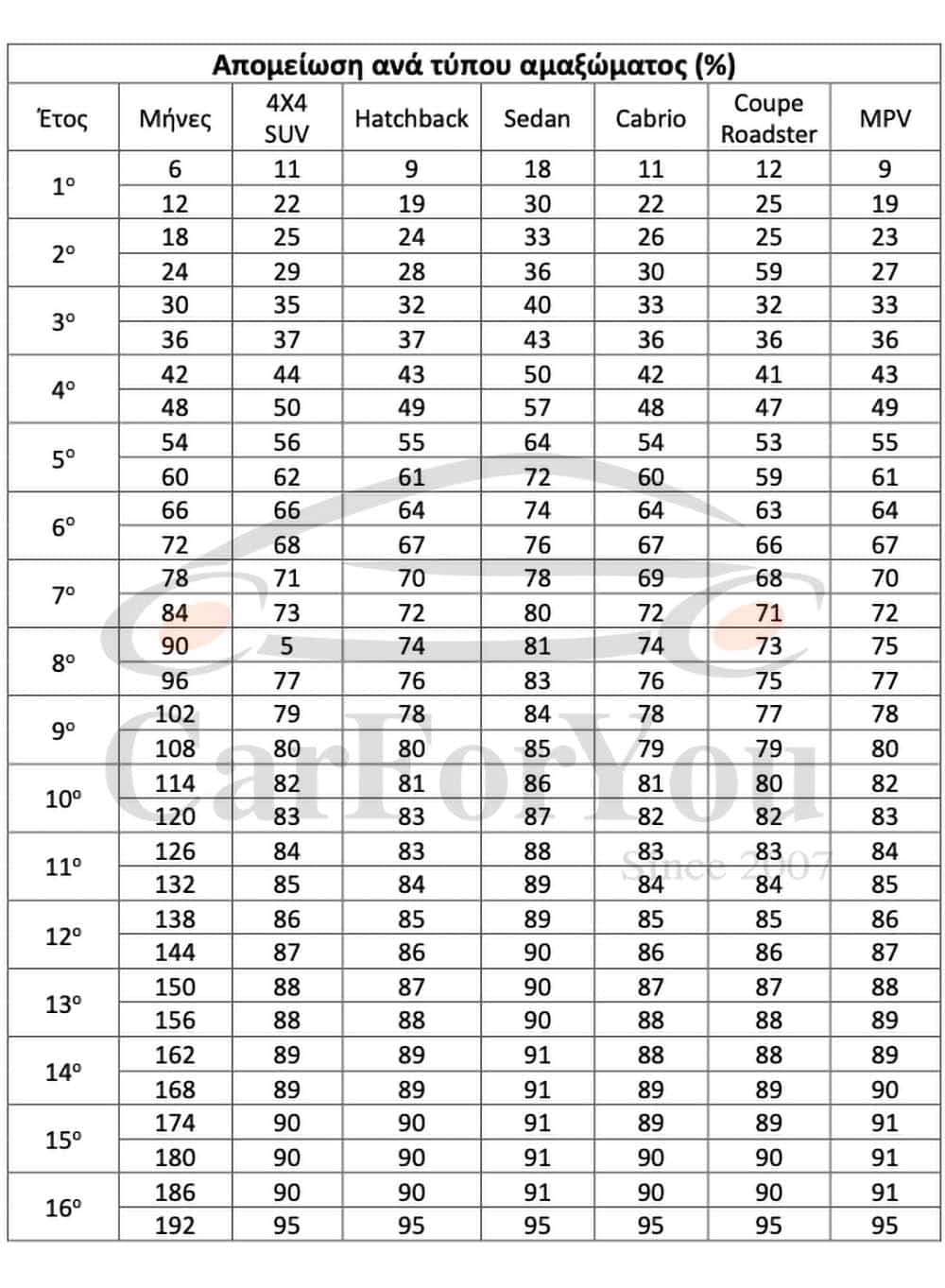

Each month of circulation depreciates the value of the vehicle, while the depreciation rate is different depending on the type of body. Below is a summary table of depreciation per half-year, the depreciation actually occurs month-by-month, so there are intermediate values between those in the table below, which are briefly mentioned in six-month increments.

Kilometers driven reduce customs clearance costs when they are more than 15,000 km per year. For every 500 additional kilometers over the average 15,000, its taxable value is reduced by 0.1%. Maximum mileage impairment is 10%

The calculation of any reduction in the registration fee that may arise due to mileage is made based on the purchase invoiceof the car, when importing the car, and not the kilometers indicated on the odometer. That is, if we buy it with X kilometers, transport the car by road and finally import it with X+2,000 kilometers, then when calculating its registration fee, the customs office will take into account the kilometers indicated on the invoice and not the final kilometers that it will have on the odometer.

Motorhomes pay a quarter of the customs duty they would pay if they were just passenger cars.

VAT:

Used cars pay VAT either in the country of export or in the country of import. In the case of importing cars, it is in our interest that VAT is paid in the country with the lowest VAT, since in the case of cars it is not refunded to the buyer. New cars are required to pay VAT in the country of import. New cars are considered to be cars with less than 6,000 kilometers. and first registration certificate less than 6 months old. Both of these conditions must apply, i.e. if a car is 7 months old and 5,000 kilometers old or if it is 10,000 kilometers old and 5 months old, then it is considered new in both cases.

In the event that someone pays VAT on a new car in the country of purchase and then imports it, they will be required to pay it back with 24% on the net purchase price of the car, while they will not get the VAT paid back from the country of purchase.

No, it doesn't affect it, The value that will be used as the basis for calculating the registration fee is the retail value before taxes (LTPF) which is equal to the value of the basic version and the cost of its additional equipment.

You can calculate it based on the instructions above. However, it is complicated, it is very possible that you will make a mistake, so it is better to contact us, through our contact form, and we will calculate it for you at no cost.

Categorically not, There is no correlation with the engine capacity in the calculation of the registration fee. The engine capacity of a car affected the customs duty that an imported car, new or used, would pay under the previous legislation which has been changed for over 10 years. Do not trust online automatic registration calculators which ask you to fill in the engine capacity of the car. This is an indication that they are probably not properly informed.

The usual time required for customs clearance of a car is approximately 3 working days. Of course, there are also cars with particularities where it can be significantly delayed. For example, a car from a company that has never been imported into our country. In this case, as the retail price before taxes, we take the corresponding price it had in a European country where it had been imported and sold.

Speaking of a specific car, specific equipment (and therefore LTPF) and pollutants, the ones that have the greatest impact are:

The maximum profit you can get when buying a car with high mileage (over 15,000 km per year of use) it is 10%. The amount you will save is usually negligible compared to the wear and tear of a car with a lot of mileage. Choose the car with the fewest mileage based on the amount you want to spend.

People who tell you that the car actually has fewer kilometers than listed in order to pay lower customs duties are almost certainly making fun of you.

The price at which a similar car was sold in Greece on the date of first release.

Cars with older anti-pollution technology have increased coefficients.

Grams of carbon dioxide affect the final tax rate.

Each month of circulation reduces the taxable value of the car.

31/8/2018 – Today

Basic factors

31/8/2015 – 31/8/2018

+50% on the basics

31/12/2012 – 31/8/2015

+100% on the basics

Before 31/12/2012

+200% on the basics

Not subject to registration fees

They pay half the registration fees

They pay a quarter of the fees

They pay a quarter of the fees

Automobile VAT:

Impairment:

Environmental Fees:

CO2 Additional Fees:

Send us the model, year, cubic capacity, CO2, mileage and purchase price so we can guide you on registration fees, customs clearance and total import costs.

Request an estimate Call us